Why I Started HousePlant 🪴

Early in the pandemic, my wife and I left our tiny apartment in San Francisco and bought our first home: a charming old craftsman in Sacramento. The move allowed us to be closer to family and to work remotely more effectively. Now that we own a home, we are excited that our monthly housing expenses are building equity instead of paying off our landlord’s mortgage. Fixing up an old house has been a great hobby during the pandemic. We learned new skills from hardwood floor restoration to appliance installation to laying sod.

We love our sweet home, yet there is an important reality we had to face in order to buy this house: we had to leave our beloved San Francisco where we’d lived for over 15 years. We saved diligently, but we would have never been able to save up a 20% down-payment on an SF property where the median value is ~$1.2M.

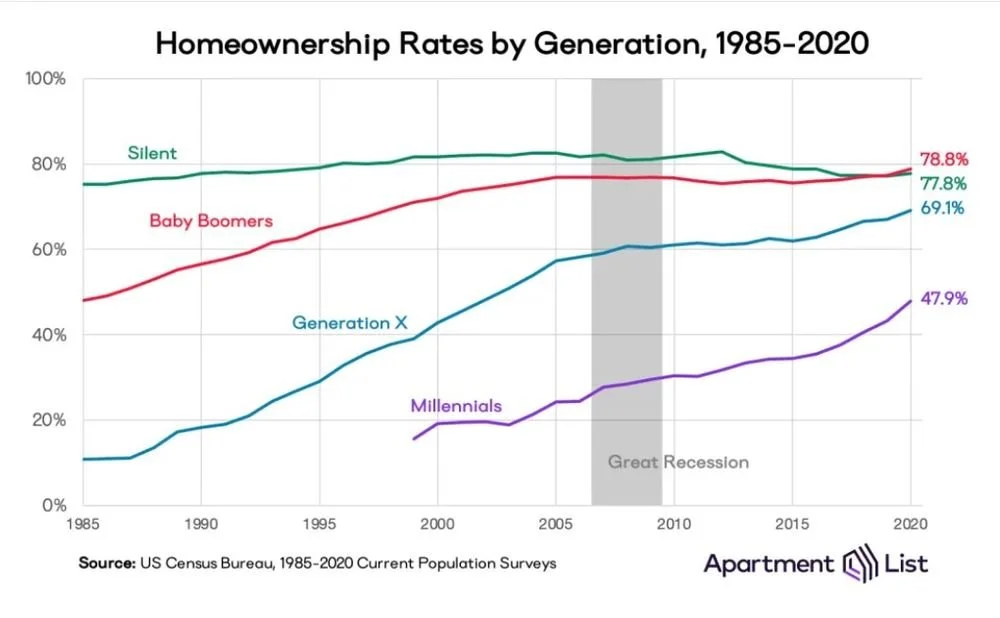

Out-of-reach down payments aren’t just a barrier in the most expensive markets like San Francisco, the rise of median home prices compared to median income is happening all over the country (and has been growing steadily for the past 50 years). The effect of this is showing up in census data as well: Home-buying amongst younger generations is way, way down. Lower rates of home ownership for younger generations increases our risk of expanding wealth gaps and increasing inequality across the country.

What can be done?

To start, we need to make down payments more realistically achievable in today’s economy.

I’m excited to share a new platform I’ve built to facilitate social loans: a new, easy way for people to request + lend each other funds for down payments. I couldn’t be more excited to be getting closer to launching HousePlant and start working with homebuyers.

HousePlant offers an easy, secure, and reliable way to crowdsource down payment loans from people you know.

The power to build home ownership and economic independence is right here in our own communities. Here’s why this is important:

“At age 35, millennial home ownership hit 53% compared with 60% for Gen Xers and baby boomers, and almost 70% for pre-boomers.”

Less than 48% of U.S. millennials owned homes in 2020 according to U.S. Census Data.

What is the culprit behind lower home ownership in younger generations?

The down payment is too high!

According to a related Apartment List survey, 74% of millennials say that they cannot afford to buy a home. 63% of millennials have no down payment saved.

And this isn’t because we blew all of our money on avocado toast either…Home prices relative to wages are significantly higher than they've ever been, and this makes it difficult for people to save up a big down payment. Without 20% down, homebuyers usually pay higher interest rates and PMIs (private mortgage insurance), or lose out on home buying completely.

“After accounting for inflation, home prices have jumped 118% since 1965, while income has only increased by 15%, according to a separate report based on Census data.” - Jessica Dickler, CNBC

This is an important problem to solve, because preserving home ownership is one of the most effective ways to combat long term inequality. The disparities above become even more stark with regard to race: Black millennials face the lowest rate of homeownership and the largest gap between generations.

Creative, flexible new financial solutions will outcompete outdated models that reinforce inequities.

Time and time again, from housing to social movements, people collectively expand power through community: let’s use it to create new financial models which build localized income through Social Loans.

What are Social Loans?

Social Loans are flexible, customized loans from people you know.

People are accustomed to crowdfunding, P2P payment apps like Venmo, and wedding registries. Yet when it comes to home-buying, often our single largest lifetime purchase, there haven’t been services that make it easy to ask for help (or pitch in for someone you care about)… until now.

HousePlant makes it easy to crowdsource loans from people you know.

You create your own unique Ask Page detailing your home-buying goals. When you share this on social media, friends and family can view your page (similar to a crowdfunding-style interaction) but instead of donating small amounts of money, they can create a customized Loan Offer and specify terms like amount, interest rate, and payback preferences. When the Borrower and Lender agree on an Offer, HousePlant helps them solidify and track their agreement with a digital signature, simple PDF records and tips to support financial transfers and paybacks.

Agreement documentation on HousePlant is great for borrowers because they can use this with their mortgage lender and offers peace of mind for lenders who no longer have to worry about the awkwardness and relationship-straining requests for repayment. What a relief.

The Future of Social Loans

Let’s face it: everyone either has or has heard a cautionary tale about loaning money to a family member or friend. Unpaid debts have strained countless relationships, largely because there is seldom documentation and transparency of the agreement.

But it doesn’t have to be like this. With social loans, agreements are written and the terms are clear. Millions of dollars are already loaned socially every day. With an easier facilitation process via HousePlant, this can become so much less stressful and so much more empowering to everyone involved. Plus- how great would it be for the interest on some of your loans to stay local and go to someone you actually know?

I believe social loans will be a major finance trend in future years.

After spending over twelve years at the intersection of technology and social change, I’m more resolute than ever that the most significant social impact tools are those that unlock the widest range of new possibilities for the widest group of people. I’m truly excited to see where this financing model leads and what possibilities it creates.

After the last couple of years, I hope you’ll agree: It’s time for more happily ever afters. Buying our first home was part of ours. I hope to offer a great tool to help you write your next chapter. Happy HousePlanting! 🪴